We meet at end of the year, and it is the right time to look back at what we have achieved and to point out future challenges.

Several signs of imbalances in the Latvian economy can be observed; to resolve them, structural reforms and decisive action are necessary, in particular to avert strain in the labour market. At the same time I would like to remind you of the need for a balanced budget, promised already such a long time ago.

But let's start with the euro area economic trends.

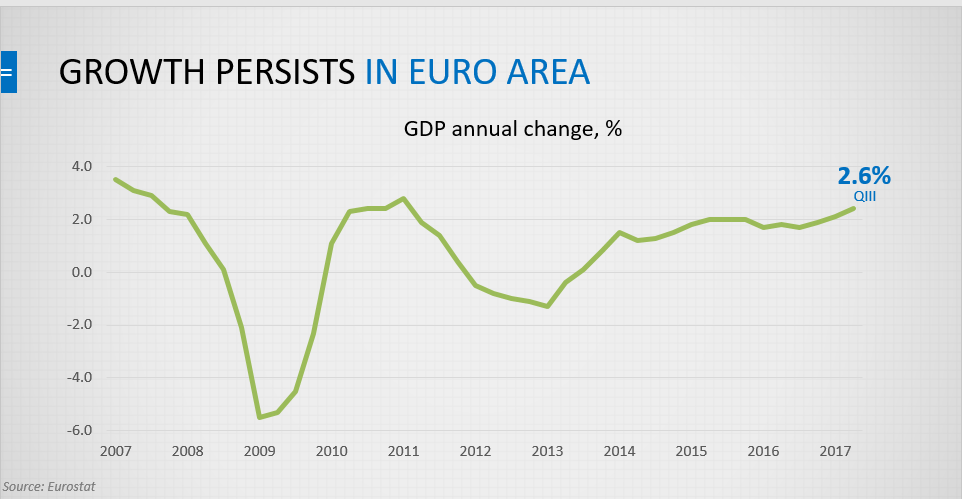

The euro area saw 2.6% economic growth in the third quarter this year, slightly higher than projected.

The euro area economic growth was supported by very favourable financing conditions further strengthening domestic demand. A rise in employment strengthened private consumption; moreover, improving corporate profitability and availability of external financing were drivers of investment growth. Strong global trade growth had a positive effect on the external demand in the euro area.

In November, the euro area inflation rate stood at 1.5%, 0.1 percentage point higher than in October. An accelerated rise in energy prices accounted for the above increase in inflation. In November, core inflation, excluding the impact of the volatile energy and food prices, remained unchanged at 0.9% month-on-month. Yet, it is a decrease in comparison with the September rate of 1.1%. The fall resulted from an unexpectedly lower rise in prices for services.

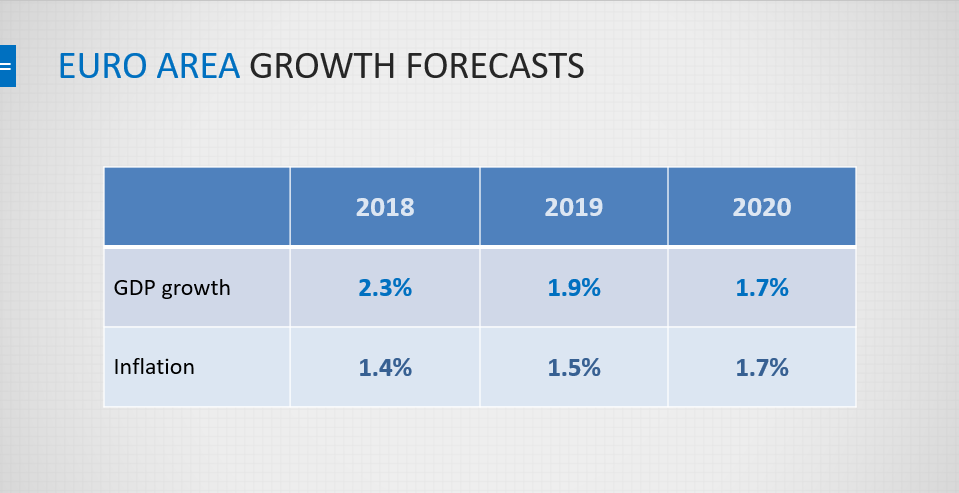

Yesterday, on 14 December, the Eurosystem released its latest macroeconomic projections for the euro area. According to them, euro area GDP growth will remain strong and the growth projections have been revised upwards over the whole projection horizon.

According to the projections, the euro area economy will grow by 2.4% in 2017, 2.3% in 2018, 1.9% in 2019 and 1.7% in 2020. The accommodative monetary policy, improvements in the labour market and the favourable external environment will continue to support economic growth.

Inflation forecasts have also been revised slightly upwards, mostly on account of higher oil prices. A rise in wages and salaries, driven by the increasing shortage of labour force, in the major economies in particular, is also expected to support price rises.

According to the projections, in the euro area inflation is likely to reach 1.5% in 2017, 1.4% in 2018, 1.5% in 2019 and 1.7% in 2020.

Let's proceed with developments in the Latvian economy.

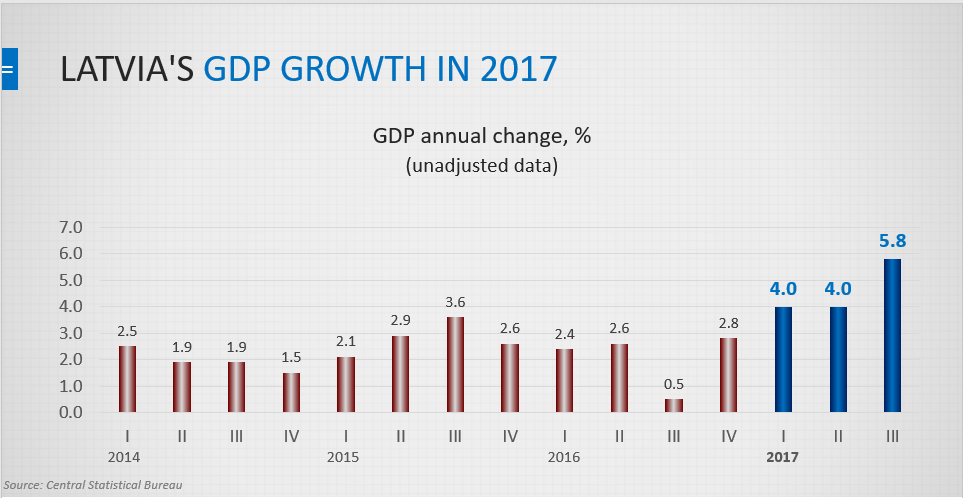

The persistently accelerating growth rates of the Latvian economy notwithstanding, the growing shortage of labour force, discussed already in the press conference in September, is observed along with an increase in investment and purchasing power. The shortage makes a pressure on wages and prices resulting in an adverse effect on the competitiveness of Latvian businesses. Weaker competitiveness in its turn means a likely moderation of the Latvian economic growth in the medium term.

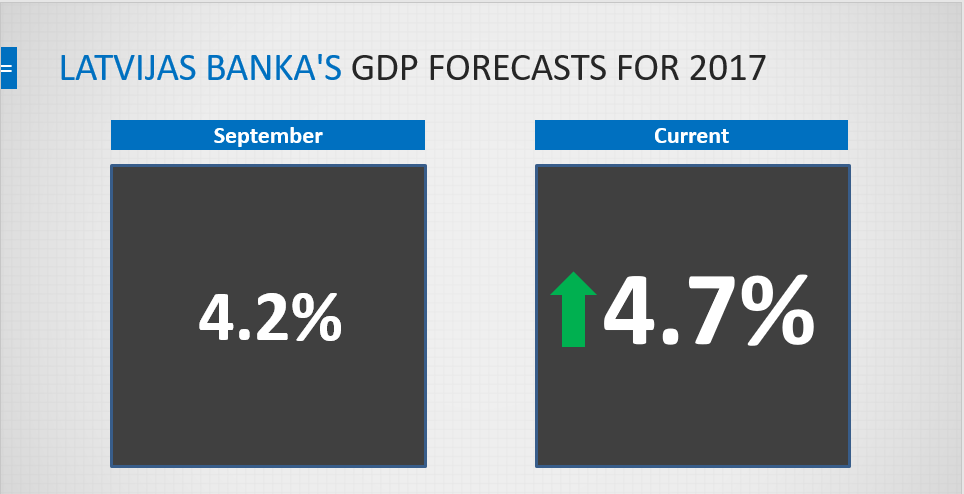

Speaking about the annual forecast, we can see that in 2017 the growth of the Latvian economy was faster than expected on account of stronger external demand, larger investment and private consumption. In view of the above factors, GDP forecast has been revised upwards from 4.2% to 4.7%.

It should be noted that robust economic growth can be expected also in the future; nevertheless, it will slow down, with the external demand, and investment posting more moderate growth. In 2018, GDP growth is likely to stand at 4.1% (3.8% according to our previous forecast).

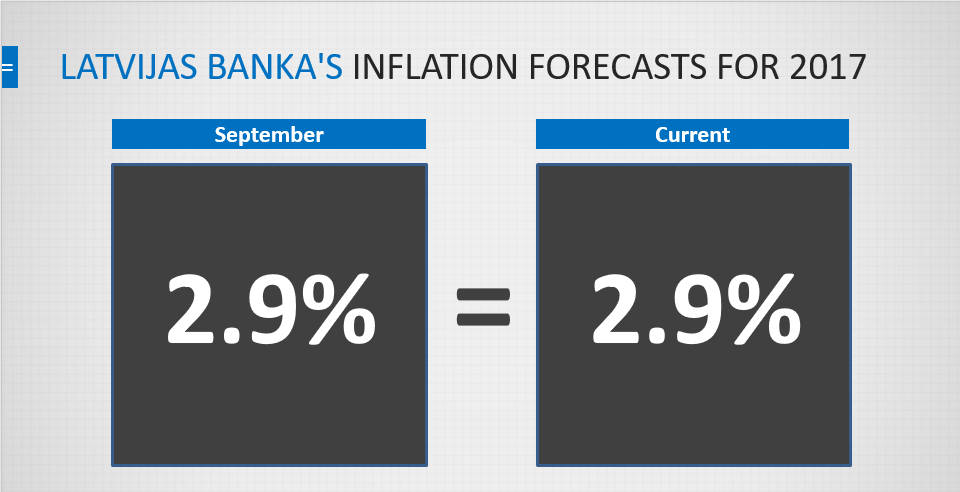

The inflation forecast remains unchanged at 2.9% for this year. The oil price dynamics slightly exceeded the forecast, but this effect was offset by the appreciation of the euro vis-à-vis the US dollar. As to the inflation forecast for 2018, based on the analysis of the oil price developments, expected economic activity and potential labour shortage, Latvijas Banka's inflation forecast remains at 2.9%.

In the last press conference, I made an in-depth analysis of the current temperature of the Latvian economy. There are several signs that have served as a basis for starting a discussion on whether there are overheating risks in Latvia now.

The situation is absolutely different from the one experienced during the previous crisis: inflation levels are under control, the lending growth is still weak, we have a low current account deficit, and growth is two times slower than in the pre-crisis period.

However, several signs point to serious problems that might have a significant impact on the competitiveness and growth potential of the Latvian economy in the future.

Therefore today I would like to highlight those things, homework, that, we believe, has to be done so that we are not trapped in a period of slow growth in the future.

During the fat years, the excessively strong growth of demand was the problem and the economy needed to cool down. Currently, the situation on the supply side or availability of labour is the reason for concern. It means that this time measures ensuring availability of labour to businesses should be implemented rather than restraining lending growth and consumption.

In the absence of action, Latvia will lose its competitiveness and growth will decelerate. Our concerns are confirmed by the development of several indicators, for example, the shrinking of the export market share signals weakening of competitiveness.

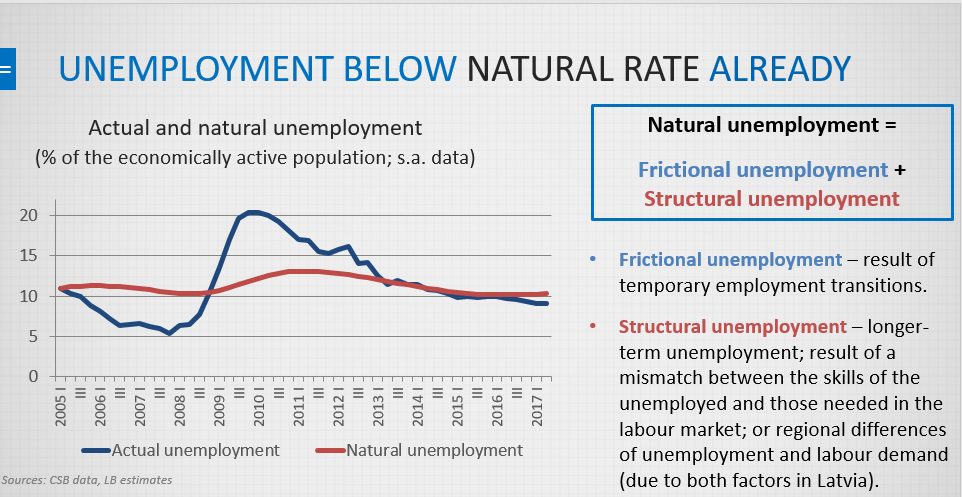

Moreover, unemployment in Latvia has already sunk below its natural rate. This results in an increasing pressure on wages, higher business costs and lower competitiveness.

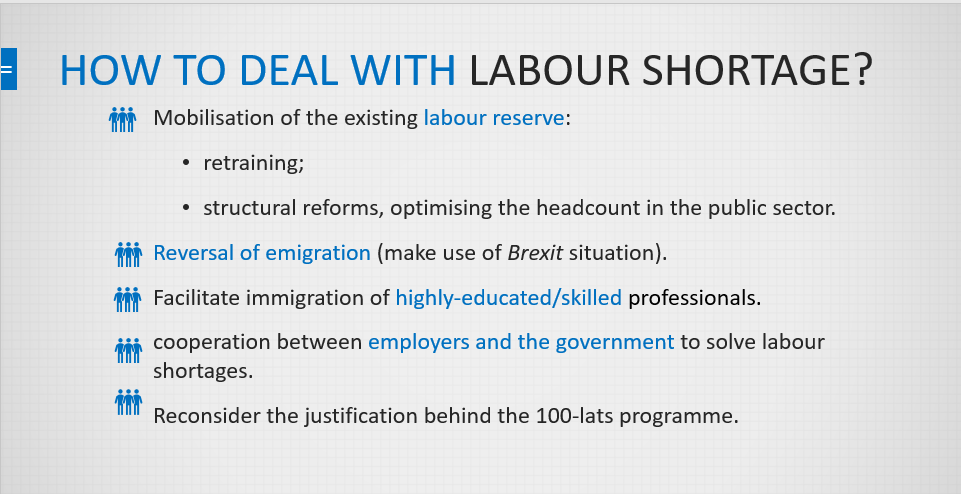

It is high time to look for an answer to the question of how to deal with the shortage of labour.

We propose the following: mobilisation of the existing labour reserve; retraining; promoting mobility; structural reforms optimising the headcount in the public sector; reversal of emigration, for example, using the new situation resulting from Brexit.

Immigration of well-educated and highly-skilled professionals should also be facilitated and cooperation between employers and the government to solve labour shortages should be established. The justification behind the so-called 100-lats programme should also be reconsidered.

Active work has already started in some of those areas. For instance, the public administration reform envisaging an annual 2% decrease in the headcount in public administration, proposed by the State Chancellery and supported by the Cabinet of Ministers, is a positive initiative. This will be a great support in circumstances of a fairly tight labour market.

Unemployment is the highest amongst low-qualified population and their training, retraining and return to the labour market is a significant task. Unfortunately, Latvia does not spend much on retraining the unemployed and is more focussed on less effective labour market policy measures.

The number of unemployed persons involved in vocational training and mobility measures should be increased significantly.

The structural reforms that have been launched in the sectors of education and health care should also be continued. Let me remind you that the delays in the implementation of the structural reforms is the very reason why we have to speak about signs of overheating already at 4%–5% economic growth.

Let's turn to the fiscal policy.

I am not going to analyse individual taxes of the budgetary system this time. I would like to stress only one important thing which Latvia has failed to learn from the previous crisis. Namely, in an economic upswing a surplus budget or at least a balanced budget should be formulated, instead of increasing the government deficit. Then, if the next crisis comes around, there would be no need to cut spending Latvia can no longer finance again unless we borrow huge amounts of money, increase Latvia's debt burden and costs of its servicing.