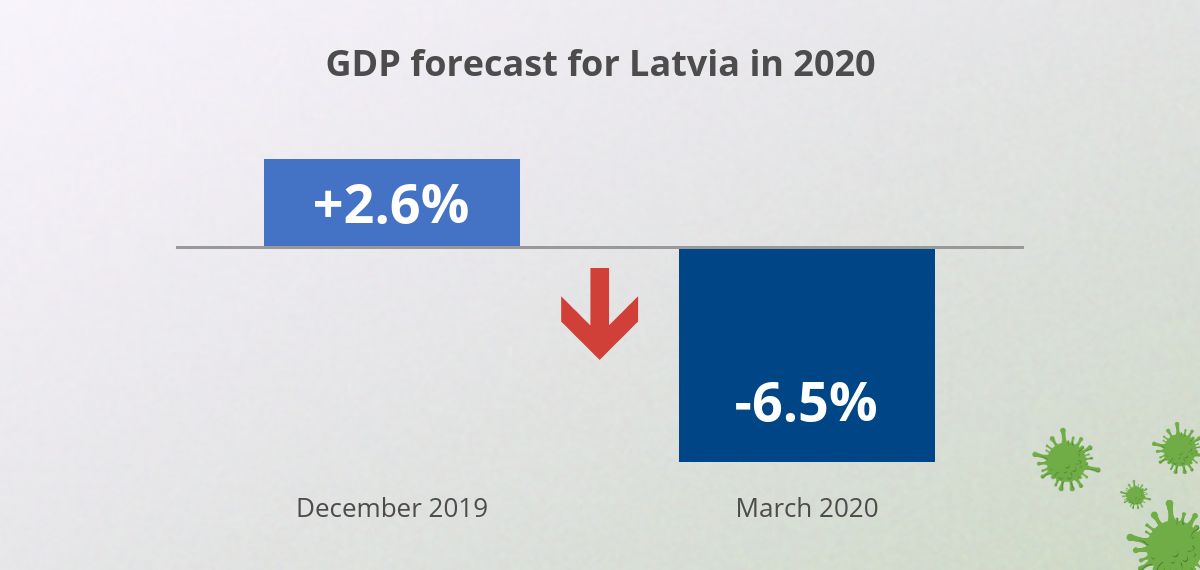

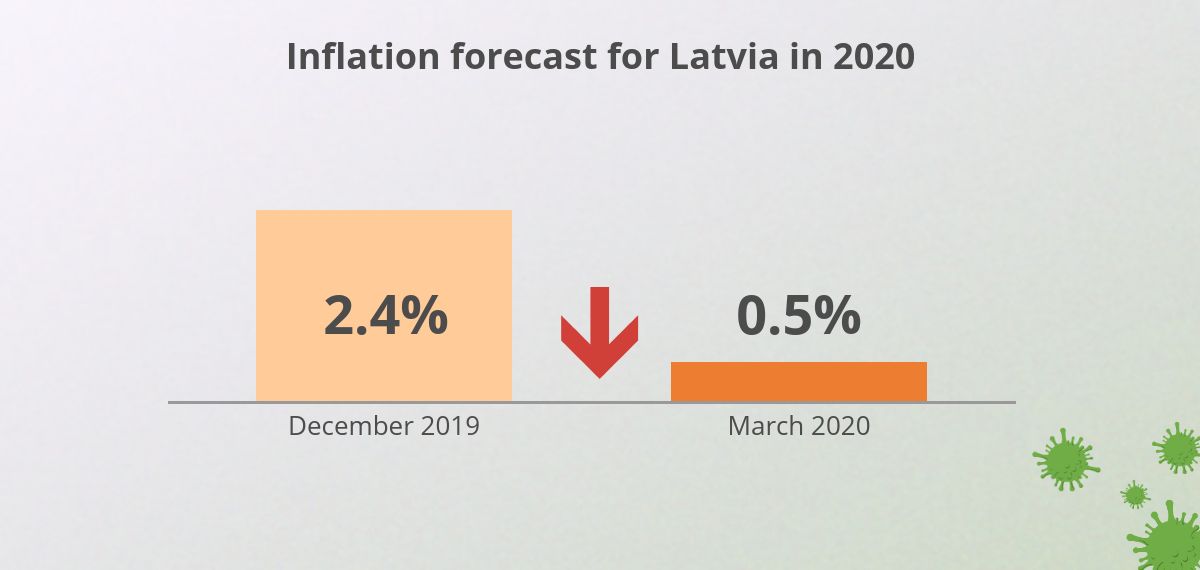

Latvijas Banka has revised its gross domestic product (GDP) and inflation forecasts for Latvia. Considering the latest global economic developments, including the implications of the outbreak of coronavirus COVID-19, Latvijas Banka has revised downwards its forecast of Latvia's GDP growth for 2020 to –6.5% and that of inflation to 0.5% (2.6% and 2.4% in December 2019 projections accordingly). Moreover, in view of the heightened uncertainty surrounding the forecasts, they may be subsequently adjusted significantly in case of delayed progress in limiting the spread of COVID-19 worldwide and economic growth failing to restart in the second half of the year.

According to the assessment of Latvijas Banka's economists, the rapid spread of COVID-19 has resulted in high uncertainty and substantial deterioration of the global market sentiment as well as significant business disruptions, thereby enhancing the probability of a global recession. The global economic implications will largely hinge on the spread of the coronavirus and the scope and duration of the restrictions to combat the virus; these negative effects will be partly offset by the announced sizeable national fiscal policy initiatives in combination with the highly-accommodative monetary policies implemented by the central banks.

International assessments concerning the global economic consequences of COVID-19 and country effects vary; nevertheless, they point to a significant weakening of the economic activity and are becoming increasingly more negative. The range of projections is extremely wide, depending on the experts' assumptions concerning the speed of limiting the virus spread. The IMF projects negative global economic growth this year, and expects that the fall will be, as a minimum, of a magnitude of a global financial crisis. Moreover, the latest market forecasts of the euro area growth range from –5% to –1.7%.

Such adverse global shock creates immediate cash flow problems to businesses that may lead to solvency issues at a later stage as they fail to meet their obligations. Targeted support measures implemented by the Latvian government are crucial for mitigating the consequences of the crisis, so that the short-term business disruptions would cause no significant loss of the economic capacity that could delay the recovery after the virus spread has been stopped, thereby exerting a lasting downward effect on the economic activity. At the same time, it is important to extend support to those affected by downtime and having lost their income, in order to prevent a significant build-up of social problems and contraction of domestic demand.

The currently-announced government measures are a step in the right direction, yet they need to be commensurate with the magnitude of the crisis and targeted at businesses and households hit the hardest. They should cover a wide range of economic sectors and be limited to the duration of the crisis. The European Commission has announced a temporary suspension of the fiscal rules, providing national governments flexibility with regard to their budgetary spending to mitigate the negative consequences of the crisis. The European Union rules on state aid also enable the Member States to provide fast and effective financial support to businesses. Latvia has been fiscally responsible, keeping its sovereign debt at a relatively low level; therefore, it is able to provide the necessary support to the economy in times of a crisis. Moreover, the current situation is fundamentally different from the 2008–2009 crisis when spending cuts were required. This time, thanks to observing fiscal discipline over the previous years as well as due to balanced economic development and absence of macroeconomic imbalances, Latvia is able to borrow in order to support the economy.

Our macroeconomic projections reflect an economic development scenario assuming negative effects of the coronavirus over the first half of the year and a relatively quick recovery of the economic activity thereafter. The state of emergency declared in Latvia as well as in other countries and the implemented social distancing measures required to contain the spread of COVID-19 have a significant downward effect on the economy already now. The restrictive measures have already shut down business activity in selected sectors in Latvia. Yet the implications will be negative for most sectors of the economy via supply shocks (disruptions in logistics and intermediate supply chains and rising costs) as well as external and domestic demand and confidence shocks.

On the backdrop recent developments, we expect GDP contraction of 6.5% in 2020.

- This projection hinges on the assumption that the spread of the coronavirus will be contained rather successfully and hence its effect on the economy will be short-lived. Economy is expected to contract already in the first quarter of 2020, and the fall will accelerate significantly in the second quarter. Nevertheless, it is expected that the economy will start to recover in the second half of the year, with global demand for goods rebounding and the delayed domestic consumption resuming. At the same time, investors could remain cautious for a longer time.

- The ban on public events and gatherings as well as mobility restrictions paralyse the activity of several sectors directly and immediately. The drop in value added in accommodation and catering, recreation and entertainment services can be estimated at 70% in the second quarter, and at about 30% in 2020 overall.

- Transport services are significantly affected by the suspension of international passenger transportation as well as the decline in freight transportation by road due to precautionary measures and delays in transportation of container cargoes. Hence, we expect a fall of roughly 20% in this sector for the year overall.

- COVID-19 will have negative implications for a broad spectrum of sectors. Manufacturing will also experience contraction, initially due to supply chain disruptions and subsequently due to the resulting shrinkage of demand. Only some narrow sub-sectors are experiencing higher demand; therefore, both the domestic market oriented manufacturers and exporters are bound to suffer. Production of goods can be expected to rebound vigorously in the second half of the year on the back of recovering global demand, inter alia considering the depletion of inventories during the crisis period and the need to rebuild them later on.

- Trade, which is a large sector of the economy, will contract on account of shrinking retail trade due to the introduced restrictions, expected decline in household income and consumption, despite the resilient demand for food as this accounts for merely 40% of the retail turnover. The sector will be also affected by the problems of the wholesale sector caused by the above-mentioned falls in container cargo transportation and overall demand.

- Meanwhile, investor cautiousness will also find reflection in a declining contribution by the real estate and construction sectors. The above sectors have been affected by other factors as well, e.g. delays in building material delivery and unfavourable income and lending dynamics.

The unfavourable impact on a wide range of sectors will also drastically worsen the situation in the labour market. However, in view of the government support in easing the cost burden of businesses, inter alia providing for downtime benefits, and the substantial, albeit short-term, fall in economic growth, as projected in the scenario, the impact on unemployment growth has been assessed to be considerably smaller in comparison with the previous global crisis. At the same time, a lot of businesses will optimise their costs, including labour costs, thus the wage growth is expected to stop in annual terms, as opposed to a 7% rise in 2019. This, together with employment decline and estimated increase in the number of unemployed by around 20 thousand persons will be reflected in a drop in consumption, likely to be further dragged down by consumer cautiousness associated with the high uncertainty.

Inflation is projected to slide down close to zero, particularly in the second half of the year (averaging 0.5% in 2020), as a notable price dampening effect has been caused initially by the drop in oil prices as a result of the spread of the coronavirus and the projected fall in global demand, and later in March intensifying due to the so called oil price wars. A drop in domestic prices is expected as a result of subdued economic activity and a decrease in income. Although an upward pressure on the prices of industrial goods could be observed due to substitution of Latvia's imports from China and supply chain disruptions, they are unlikely to offset the price decline as the demand is weak.

Should the combat of the coronavirus spread take longer, the economic outlook could further worsen considerably, and risks to the growth projections are tilted to the downside. Nevertheless, given the overall good health of the economy with no persistent macroeconomic imbalances by contrast to the previous global crisis, implementation of government support measures to the extent proportionate to the problems caused by the crisis will help to mitigate the notable damage of the COVID-19 crisis caused to the economy.

More detailed information about the latest forecasts is available in macroeconomic forecasts section of Latvijas Banka's website macroeconomics.lv.